Login to view your Fidelity account(s) and access your electronic documents and statements.

Login to view your Charles Schwab account(s) and access your electronic documents and statements.

Quarterly Investment Foundations First Quarter 2026

January 26, 2026

-

Calvin D. Wiersma

Calvin D. Wiersma

MST, CFP®

Senior Financial Advisor, Director of Planning and Investments

Mastering The Subject

A Balanced Portfolio is Boring

A balanced portfolio is boring. Investing is not about winning the lottery despite what the news and latest prediction market platform tells us. It takes discipline and time to realize the benefits of long-term investments in equity and fixed income assets.

Even though equity and fixed income returns were above average last year, the results offered a stark reminder that a diversified portfolio structured to capture higher expected returns is an essential foundation to growing wealth — even if it is “boring.”

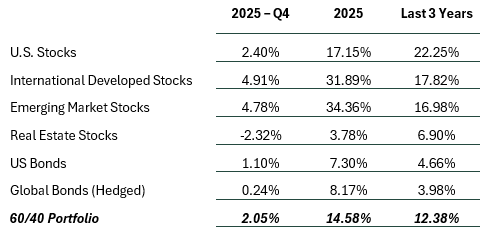

2025 Recap: Broad Gains for Global Investors

Last year, global stock markets delivered strong results. Investors with well-diversified portfolios holding U.S., international, and emerging market stocks were rewarded for staying globally balanced rather than concentrating in a single sector or region.

Fixed income also had a standout year. As interest rates declined slightly, bond prices rose, providing welcome gains for investors. Real estate, on the other hand, lagged other major asset classes.

Data as of 12/31/2025. Past Performance is no guarantee of future results. Returns shown do not include potential advisory fees. U.S. Stocks, International Developed Stocks, Emerging Market Stocks, Real Estate Stocks represented by Russell 3000, MSCI World ex USA, MSCI Emerging Markets, and Dow Jones US Select REIT indices. U.S. bonds and Global bonds represented by the Bloomberg U.S and Global Aggregate indices. The 60/40 Portfolio refers to a portfolio that holds 60% stocks and 40% bonds and is a calculated representation of the categories and their performance noted above.

What to Expect in 2026

Our focus for the year ahead is on building portfolios that can succeed through a range of economic and market conditions — not just those we expect or hope for. Here is what we are watching:

Valuations for U.S. Stocks are High

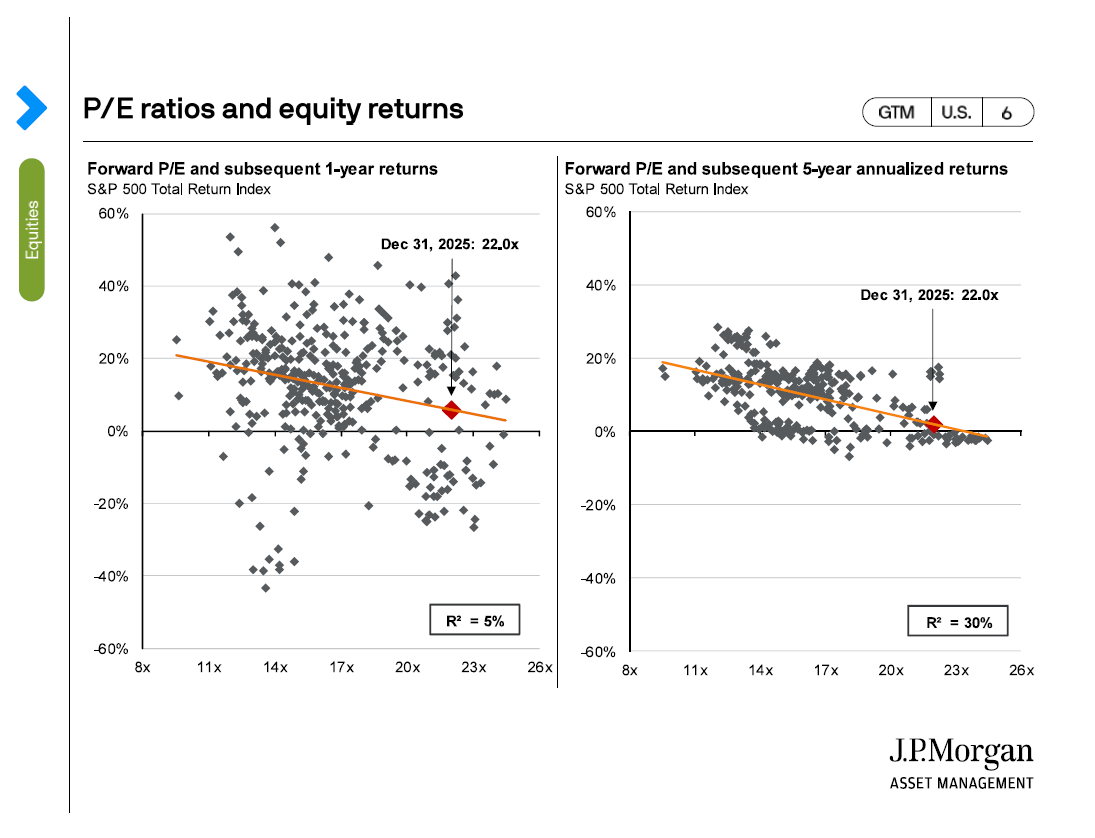

Stocks in the U.S. continue to have valuations that sit well above historical averages. As of the end of the year, the price to earnings ratio for the S&P 500 was 22 versus the 25-year average of 16.3. While this doesn’t necessarily mean poor performance in the short term, history shows that current valuation levels tend to have a predictive relationship with future returns, particularly over five years or more. You can see in the chart below that valuations only predict about 5% of the next year’s performance, but that jumps to 30% for the next 5-year period. Our key takeaway is that we can't predict what short-term returns will be, therefore we will maintain our current target allocation to U.S. equities and be positioned for long-term success.

Source: FactSet, Refinitiv Datastream, Standard & Poor's, J.P. Morgan Asset Management.

Returns are 12-month and 60-month annualized total returns, measure monthly, beginning 12/31/1993. R2 represents the percent of variation in total return that can be explained by forward P/E ratios. The forward P/E ratio is the most recent S&P 500 index price by consensus analyst estimate for earnings in the next 12 months, provided by IBES since December 1993 and FactSet since January 2022. Past performance is no guarantee of future results. Guide to the Markets - U.S. Data are as of December 31, 2025.

Global Stocks Offer Relative Value

International and emerging market stocks are still trading near their long-term averages. That was true entering 2025 and remains the case today. These more reasonable valuations coupled with a declining U.S. dollar which creates a tailwind for non-U.S. investments could lead to better returns than U.S. stocks in the years ahead. Since the policies and circumstances that may change these conditions are difficult to predict, we are maintaining our current target allocations to global markets to capture returns and manage risk.

Fixed Income is Humming Along

Bond yields have decreased slightly but remain in the 4% to 4.5% range. Historically, the starting yield on fixed income is a strong predictor of future returns. While returns may be a bit lower than in 2025, we expect returns to be higher than the latest 15-year average. With the yield curve in the U.S. steepening, holding a fixed income portfolio with intermediate-term bonds with an emphasis of investment grade corporate bonds should provide fixed income investors with dependable returns in the new year.

How We Are Positioned for the Year Ahead

As we begin 2026, we are not making changes to our long-term investment approach. Instead, we are leaning into the fundamentals that drive results over time. We continue to emphasize value stocks, especially within the U.S., where large-cap growth companies are priced at a premium. We are maintaining global diversification, knowing that attractive opportunities can emerge from any region at any time. We remain focused on what we can control: managing costs, increasing after-tax returns, rebalancing regularly, and maintaining a consistent investment strategy. These are the levers that matter most in producing better outcomes for our clients, regardless of what unfolds in the headlines.

The coming year will no doubt bring surprises. Geopolitical shifts, economic policy changes, or market swings may grab attention, but most will have little long-term impact on your financial goals. Remember, a balanced portfolio is boring, yet the results are tremendous. If you'd like to discuss your allocation or how to start building a coordinated investment plan, we are here to help.

Disclosure:

The opinions expressed herein are those of Grand Wealth Management (“GWM”) and are subject to change without notice. This material is not financial advice or an offer to sell any product. This article is for informational purposes only and does not constitute investment, legal or tax advice and should not be used as a substitute for the advice of a professional legal or tax advisor. GWM reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. This is not a recommendation to buy or sell a particular security. Past performance does not indicate future results. GWM is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about GWM including our investment strategies, fees and objectives can be found in our Form ADV Part 2 and Form CRS, which are available upon request.